Don't Get Left in the Data Dust

Modern investment vehicles, strategy & analysis

Jamie Catherwood has a fun weekly note called Financial History: Sunday Reads that uses dated publications to contextualize current market events. He also writes for OSAM and his latest piece is the first of the a three-part series on the evolution of risk management. Typical of Jamie’s style, the article makes impressive use of old media to communicate his perspective. He quotes a 19th century edition of The Spectator: “The profoundest chess-player may see an inevitable mate, and yet, if the chandelier falls upon the pieces, may never win that game.”

The third option above is a rules-based approach where the objective is to increase the probability of positive outcomes, by reducing the likelihood of negative ones. Simply avoiding the exogenous risk isn’t sufficient, but combined with in-game aptitude, it improves the player’s chances of winning over skill alone. This is similar to a portfolio manager sifting through the investable universe with screens to separate the securities with desirable properties from ones he/she believes will underperform. From a behavioral economics standpoint, an analogy would be automatic deposits into a target date retirement fund to avoid the pitfalls of loss aversion & return chasing.

The price speculators are paid to take a given risk is its expected return. While potential upside entices us to invest, loss aversion is fundamental to saving too. Investors seek to preserve the buying power of their hard-earned cash by earning above the rate of inflation and investment committees scrutinize the analysis underpinning a fund’s allocation proposals. Catherwood notes:

The remainder of the piece discusses ways that novel investment vehicles have been introduced over the years to help investors “win by not losing” and subsequent installments will elaborate on developments in strategy and technology. However, we don’t have to wait for OSAM to publish because it’s easy to see these forces in action today:

Liquid Alternatives provide retail investors access to asset classes and strategies that would have otherwise been reserved for institutions or high net worth individuals. You can read more about how advisors use them here

Assets like the Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL) and Simplify’s suite of funds that incorporate option overlay strategies make it easy to add convexity to a portfolio

Technological advances have enabled the use of trading algorithms, which are effectively rules-based strategies written in code

Developments in analytics and huge repositories data of have unlocked new ways of looking at portfolio construction, asset allocation and security analysis

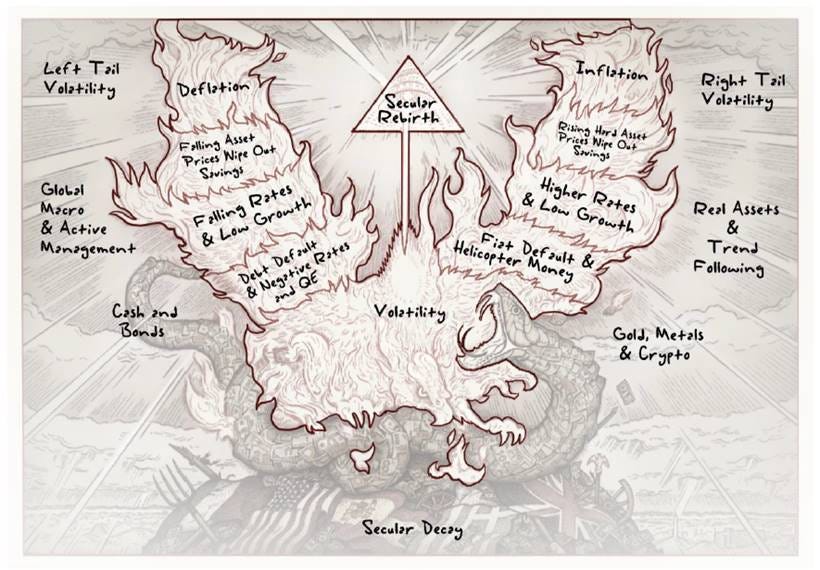

Back in January 2020, Artemis Capital published a paper that captures the themes above in the context of economic cycles. In “The Allegory of the Hawk and the Serpent: How to Grow and Protect Wealth for 100 Years”, Chris Cole details how various asset classes have performed under different economic conditions. He chose those animals because they show up across the ages in mythology as representations of spiritual conflict: “the enlightened mind of the Hawk battling the primordial Serpent of the lower self.” This is a good note on the duality paradox present within all of us and how reading can help tame the reptilian brain.

In Cole’s model of the world:

The Serpent represents a period of growth, value creation and rising asset prices. The conditions enabling this are a favorable confluence of demographics, technology and policy. However, these easy times tend to corrupt society with greed, debt expansion and eventual fiat devaluation. Previous Serpent phases include: (1947-1963,1984-2007)

The Hawk signifies the period of flux that ultimately kills the Serpent. The bird’s left-wing is analogous to a deflationary path, where an aging population slows growth and suppresses prices; leading to financial crashes and debt default. The right-wing of the Hawk represents inflation through helicopter money policies that erode confidence in fiat currencies. Eras of the Hawk: (1929-1946, 1964-1983)

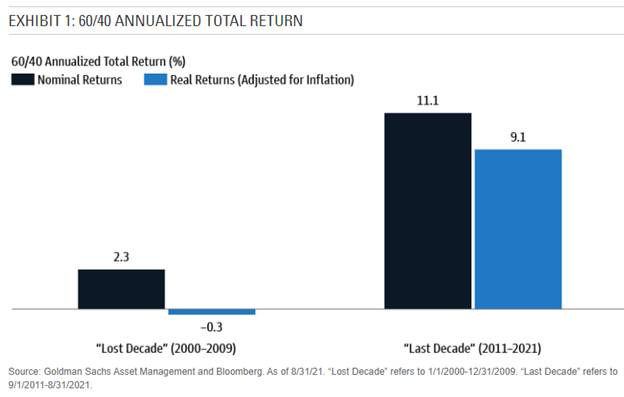

Underpinning Artemis’ view is the idea that things change and this often catches investors flat-footed due to recency bias. Following a once-in-a-century bull market in stocks & bonds, the 60/40 portfolio has become entrenched as the de facto baseline allocation, but Artemis is among many advising investors to shake things up:

The “death of 60/40” thesis is based on the idea that today’s low interest rate environment leaves little room for bonds to appreciate in value and the threat of inflation could cause fixed income to correlate positively with risk assets; leading to significant losses for the standard equity/fixed income allocation.

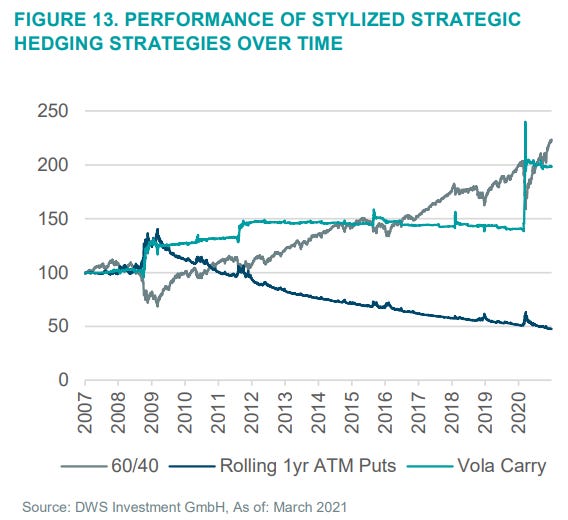

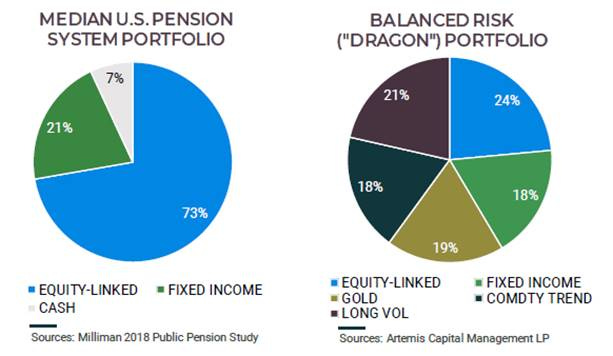

It’s a good thing that we’re witnessing so much investment vehicle innovation as it seems necessary to survive an era of the Hawk. To “win by not losing” in today’s environment, GSAM advocates for investments in infrastructure, private loans and emerging market debt as diversifiers that provide income. Artemis believes you should allocate to countertrend assets/strategies like: Gold, Commodities & Active Long Volatility. This note from DWS outlines the edge gained by including liquid alts in a portfolio and highlights why active vol strategies are preferred to passive ones:

Even if the volatility carry strategy loses money some years, the fact that it has little/negative correlation (especially in times of equity market stress) is a gift to allocators. While their performance can be spotty, these tools provide the nimble investor with tactical rebalancing opportunities into undervalued assets during a sell-off. To minimize the impact of cognitive biases, these rotation trades should be governed by a rules-based approach.

What do you get when you mix a Hawk & a Snake? A winged-serpent that balances the forces of each regime. This is what Chis Cole calls The Dragon Portfolio. It’s an elegant solution, but it’s quite complex to implement in practice:

While Chris Cole finds that the portfolio above should outperform during both secular growth & decline, it requires substantial discipline because any one of the asset classes can underperform for a long time. Remember, it’s the correlation (or lack thereof) that matters here. “The act of abandoning any of these assets, even after a decade of underperformance, destroys the point of the balanced portfolio. Very few fiduciaries understand this effect, and even fewer have the emotional and intellectual discipline to implement this portfolio.”

Shortly after the Artemis research came out, Corey Hoffstein of Newfound Research published a thoughtful paper that summarized his findings after many months spent investigating the narratives associated with “weird” market behavior. Specifically, he dug into:

The influence of central bank policies

The growing role of passive & index strategies

The liquidity mismatch between HFTs and volatility-contingent participants

I’ve recommended this paper several times in the past, so I won’t go into it with much detail. Given that a US-centric 60/40 portfolio has performed so well over the past decade, it is difficult to argue against it. However, Corey’s work leads him to believe that there’s an “increased probability of rapid market melt-downs and melt-ups.” If he’s correct, then a more thoughtful approach to the equity allocation could generate superior returns. Similar to Artemis’ Dragon Portfolio, Newfound seeks to allocate such that the portfolio can perform well in a number of different environments:

Like most industries, finance continues to mesh with technology and it’s easy to see why. The backtesting involved in the research above would have been intense. If implemented, monitoring all the necessary inputs to tactically allocate across the different buckets would require considerable modeling capabilities &/or the use of 3rd party services to crunch the figures for you. Adding to the complexity is customization - an emerging theme for maintaining client relationships. As advisors are increasingly asked to offer bespoke solutions across their book, the data wrangling liability only intensifies.

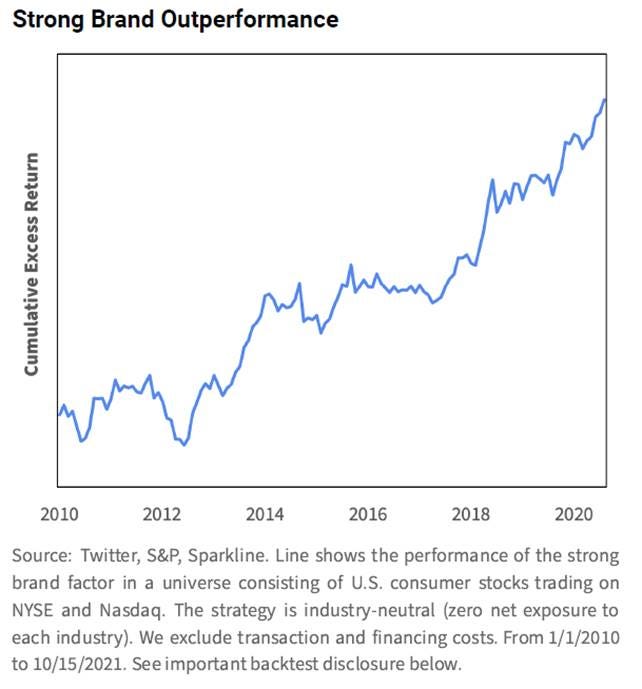

The burden of information management exists beyond broader allocation decisions too. Kai Wu of Sparkline Capital publishes occasional notes that offer a glimpse at how machine learning techniques can be incorporated into the investment decision-making process. The latest piece uses Twitter data and research from David Aaker to uncover some important traits of consumer-facing companies. The principal components below have been shown to explain over 90% of the variance in a brand’s perceived personality:

Sparkline used Natural Language Processing and clustering algorithms to categorize a universe of words/sayings according to the framework above, then mapped them to different firms. This is tricky given how much slang is used today and how it changes. Plus there’s rampant use of sarcasm on social media too… Having said that, the model seems to do a pretty good job of capturing the essence of the brand pillars, which can be used to create company profiles:

Digging into the nuances here enables Kai & Co. to track things like overlapping consumer preference changes and how a company’s mark is positioned relative to others. Perhaps most interestingly, they can test if brand strength is related to stock market performance. It’s worth digging into the detail, but effectively the exercise buys the stocks with the strongest brands and shorts those with the weakest. They also sector neutralize to ensure like-for-like comparisons. Here’s the performance:

Boom. “Strong brands are a deep moat that affords firms greater pricing power, sales volume, and customer loyalty.” Importantly, given the continued outperformance, it seems that the intangible asset is under-appreciated in the market. This exemplifies how an astute analysis using modern data wrangling techniques can produce alpha.

Is ignoring data science today like playing chess under a loose chandelier? When I started working in financial markets, quant strategy was still pretty nascent. There were some specialists on the sell side, but most chart packs tended to focus on technical analysis, seasonality and mean reversion. As computational methods moved to the mainstream and analysts have learned new skills, the frequency of seeing more modern approaches in published research has picked up. Banks & asset managers have pivoted their hiring practices to be less focused on finance/accounting and more weighted towards STEM applicants too.

Over the past few weeks, analysts on both sides of the street have spent hours poring over quarterly disclosures and updating Excel models. Do you think investment research will become less focused on backward-looking accounting & more reliant on finding an alternative edge?

Have a great weekend!