How Do You Audit a Narrative?

Accounting pitfalls, Free Cash Flow & Pushing back to get what you want

One of the knocks against accrual accounting is that, in many instances, it mistreats the time-value of money. Opportunity costs are central to the idea that a dollar today is worth more than a dollar tomorrow and of course they’re relevant for how we allocate our days as well. The US banks kicked off another earnings season this week, which got me thinking… Relative to the amount of time it takes to dig through a company’s disclosures, would investors be better served to focus their attention elsewhere?

This paper from the International Journal of Economics and Management Engineering seems to support the idea that financial reporting is losing its relevance. The analysts fail to find a statistical link between earnings beats/misses and subsequent stock movement, but they demonstrate that guidance revisions do have a significant impact on equity prices. Today, most companies emphasize adjusted figures, which fall outside the purview of IFRS/GAAP and are thus not covered by the auditor’s statement of assurance. Corporate guidance is protected under Forward-looking Information disclaimers and it’s usually made in reference to non-standard metrics anyway, which means that investors (or maybe speculators) place a higher value on unaudited/uncertified narratives.

Francine McKenna is a vocal critic of the audit process. Her newsletter, The Dig, is a good source for non-consensus perspectives on the Big 4 accounting firms and the assurance industry more broadly. Recently, she wrote about the idea that audits are largely irrelevant if commentary & momentum are the real drivers of equity performance:

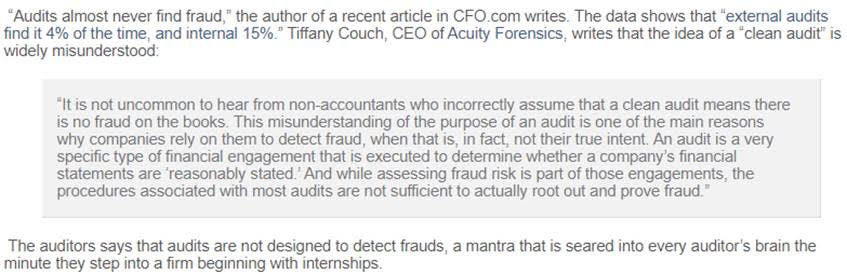

Many are already aware of this, but it’s worth reminding everyone of the following:

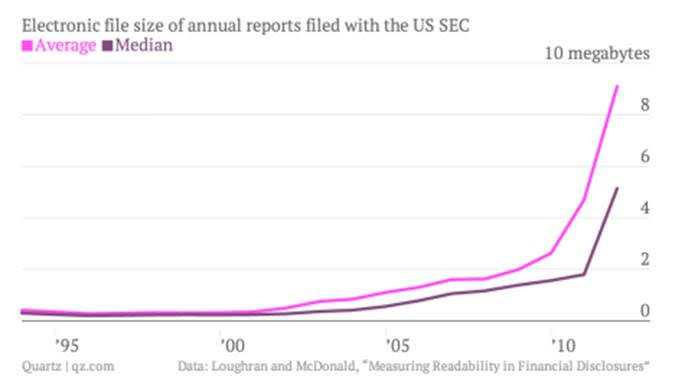

The ACFE notes that financial statement fraud is the least common incidence (10% of cases covered in their 2020 Report to the Nations) but most costly at a $954k median loss. However, the current audit practice is not optimized to uncover it. Getting back to opportunity cost… Check out this chart from Quartz showing the average length of annual reports for UK issuers (as measured by file size):

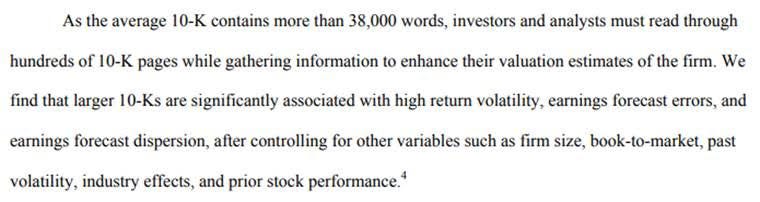

There is a tendency to think that society generally improves over earlier versions of itself, so the trend of filings getting longer is a good thing and more disclosure leads to greater transparency/decision-making, right? Not so fast. Academic researchers are at odds regarding the merits of this trend in corporate disclosures. Here’s a paper from two finance professors at Notre Dame which finds a positive relationship between the length of a company’s annual report and the volatility of its shares.

However, these researchers from Canada & the Czech Republic find empirical support for highly detailed reporting. Their models lead them to conclude that “numerical and textual information included in annual reports explains approximately 10%” of short term returns and “provide value-relevant information against which newly arriving information is more readily interpreted by investors and is incorporated more quickly into stock prices.” It appears that the jury is out in terms of the benefits associated with large volumes of information contained in issuer filings…

Another critique of current financial statement preparation is the handling of intangible assets like R&D. Using traditional accounting, these costs flow through the income statement instead of being capitalized on the balance sheet like Property, Plant & Equipment. This has the effect of reducing the issuer’s profitability and book value so companies with relatively high intangibles screen as less attractive for traditional value investors. This is particularly relevant in today’s increasingly digital world. To compensate for this shortcoming, many investors modify the standard reports. However, the specific figures that would facilitate a transformation are not typically provided, so analysts have to make assumptions when they restate a company’s financials and this can bias their analysis. Michael Mauboussin wrote an excellent note discussing this topic (I can send you a copy):

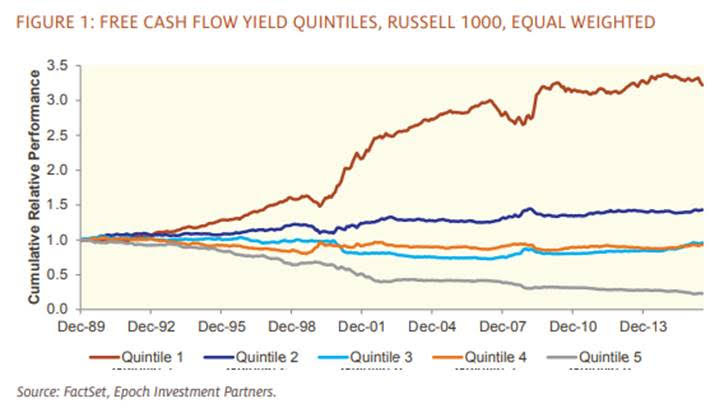

Fortunately, those who approach markets from a Free Cash Flow perspective don’t have to make changes for intangibles. The folks at Epoch Partners had a good note out the other day about the merits of focusing on FCF. The authors discuss how accrual accounting can lead to an inefficient allocation of capital due to the impacts of money’s time-value and compensation-related incentives for executives. They also highlight how historically, buying high FCF yielding companies has generated favorable returns:

Free Cash Flow isn’t a metric covered under IFRS or GAAP. Maybe that’s for the better since investors and management teams don’t agree on a common definition of the term anyways. It’s acknowledged loosely to be Cash from Operations minus Capital Expenditures, but I think working capital matters and would debate the idea that some financing charges should be included in operations, if you’d like to get into it. Despite literature pointing to the merits of analyzing free cash flows in valuation, the SEC says:

To the extent that financial statements are created with investors in mind, they seem to be falling short when addressing some of their desires. Responding to a call for input, stakeholders voiced concerns to FASB regarding earnings quality, the treatment of cryptoassets and ESG disclosure. However, the recently appointed Chair, Richard Jones’ response indicated that no changes were imminent. It’s important to be thoughtful given the sensitivity of financial information, but inaction here makes it easier for narrative to replace hard fact. We’ve seen that there is a trend towards this already, so by not adapting, are the standards boards sewing the seeds of their fading significance?

Back in 2012, the CFAI conducted a survey of its members asking “How important would each of the following potential financial reporting changes be to you in the use of financial statements?” Here’s a breakdown of the top results:

It’s interesting that the investment community places higher value on clearer disclosure while standard setters are more concerned about making the issuer’s life easier. Could this have something to do with who pays for audits?

This note from Luke Burgis provides a neat analogy of business models turning status quo on its head by way of the Japanese tradition of Omakase. In short, this is a dining experience where the guests don’t chose what they’d like to eat and instead the chef serves them a curated set of dishes. An excerpt:

Look at how the sustainability trend has taken the world by storm. Investors are consumers of financial statements and we have the potential to drive change. The accounting standards boards are slow-moving, but what if the investment industry turned up the heat? There’s a precedent for change in the air, as many groups have pushed back on an outdated status quo recently. You can probably tell that I take issue with the current audit/disclosure setup, but I’m interested to know if you agree. What friction in your process would you like to rework? Alternatively, maybe we should focus more on different data sources altogether…

“The greatest danger in times of turbulence is not the turbulence itself but to act with yesterday’s logic.”- Peter Drucker

Have a great weekend.