Is JP Morgan Chase a Media Company?

Not yet, but that's changing...

Ten years ago, Marc Andreessen presciently proclaimed that “ software is eating the world.” Eight years later, at a summit hosted by the firm bearing Mr. Andreessen’s name, general partner Angela Strange gave a presentation detailing why she believed that “nearly every company will derive a significant portion of its revenue from financial services.” Her thesis rested on the notion that the necessary “as a service” infrastructure had been built and was making its way through the increasingly software-centric technology stacks of the modern enterprise.

Nowadays, pretty much all companies contemplate “digital” in their strategic planning. Often their journey involves upgrading old systems to capture vast amounts of data, which can be used to inform internal practices and study customer behavior. Increasingly, firms are required to adopt digital identities to interact with clients, prospects, regulators and so on. A website is essential, but companies are engaging with the public and even competing on social media outlets as well:

It’s pretty cool. Today, if you have an issue with a company, you can:

Wait on hold for 20 minutes only to have the customer service rep escalate your complaint to a decision-maker, or

Send a tweet & let the heat of the public eye incentivize the company to get back to you

Operating as an internet entity requires a team with the necessary skills to create content and engage with patrons, so in a way all firms are also becoming media businesses. Maybe it’s something in the water at a16z, but here’s a thread from Balaji Srinivasan, another former general partner, who also served as CTO at Coinbase:

If we intersect this theme with the idea that “every company will be a fintech company” then it’s pretty fun to think about what the financial services industry might look like in the future.

In September, JP Morgan Chase announced their acquisition of The Infatuation - a restaurant review platform, whose mission is to: “to bring you the most honest and trustworthy opinions on where to eat around the world.” What would a consumer bank want with this asset? Well, in the words of the target’s Founder & CEO “JPMorgan Chase has proven to understand the value that high quality content and experiences can have in building strong relationships with consumers…” Boom. This is a play on leveraging favorable customer engagement to help build trust and cement long-term dealings.

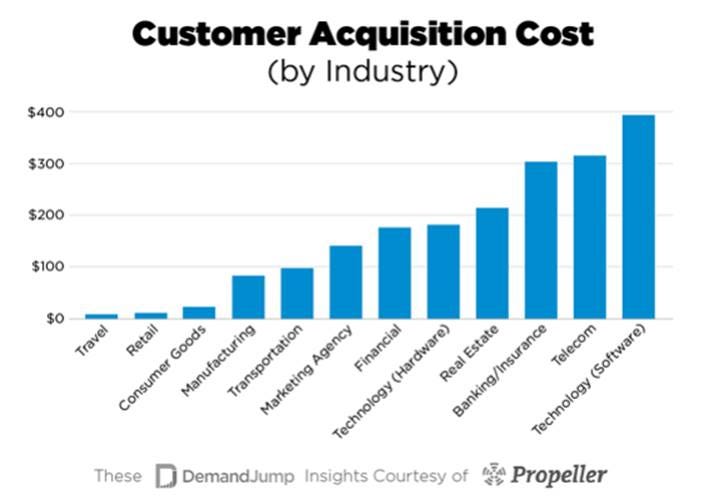

With this move, JPM has acquired the attention of 1.5M – 2M monthly visitors mainly from major cities across the US and a bunch of traffic/preference data too. The lifetime value (LTV) of a banking client relationship is relatively high compared to other industries, so competitive forces drive elevated customer acquisition costs (CAC) as well. It’s generally recognized that the opposite holds true for media companies – they have low CACs & commensurate LTVs:

CAC/LTV aren’t the most common metrics in bank analysis, but this blog post has a good rundown of why they’re important. It’s possible that the intelligence and audience that JPM acquired could drop the cost of signing new customers. You can be sure that Infatuation users are about to start seeing a lot more Chase credit cards ads. Ideally they can be onboarded to other products too.

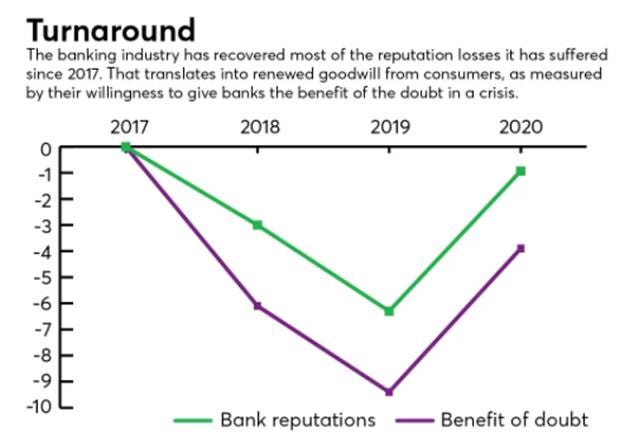

The public perception of bankers dropped after the financial crisis in 2008. While it had begun to recover, the Wells Fargo incident was another dark spot. However, the pandemic response has helped the industry’s public image:

Moves like the acquisition of Infatuation may also help JP Morgan’s image with the younger generations. Beyond capturing their attention and possibly lowering the cost of winning their business, the target also provides expertise in social media (they operate 26 Instagram accounts), custom content creation and community events with an impressive list of partners. Can this be used to deepen relationships? The company describes themselves as follows:

About a month ago, Franklin Templeton acquired O’Shaughnessy Asset Management, a quantitative asset manager with AUM of ~$6.4B for an undisclosed sum. Back in 2018, at the age of 32, Patrick O’Shaughnessy, took over the firm his father founded, but this wasn’t nepotism (you can read more here). He had a vision that custom indexing was the next big thing for investment advisors and in the short time since their related product (Canvas) was launched, the strategy has accumulated nearly $2B of assets:

Patrick said that this movement was an inevitable progression driven by lower fees for asset managers, a consumer trend towards customization and software capabilities honed over several years.

In addition to an innovative mindset & an aptitude for getting things done, Patrick brought some other assets to the helm of OSAM as well. Notably, writing skill, a book club, a podcast (one of my favorites) and more than 32K Twitter followers (O’Shaughnessy Sr. also has a considerable presence too). Fast-forward to today, the following’s ballooned to nearly 210K and the content strategy has evolved into a full-fledged media business called Colossus, whose mission is: “to become the leading destination to learn about business building and investing.”

Like banking, investment management is a trust-based endeavor so it’s interesting to see Patrick use these digital methods to increase his personal brand and by extension grow the firm bearing his name. He’s not alone in this approach either. Ritholtz Wealth Management has $1.8B of AUM and is often in the public due to the popularity of its founder (https://ritholtz.com/) and partners: Josh Brown (https://thereformedbroker.com/), Michael Batnik (https://theirrelevantinvestor.com/) and Ben Carlson (https://awealthofcommonsense.com/). These IAs each have a dedication to providing thoughtful investment-related material to the masses. The latter pair also hosts the Animal Spirits podcast, which is something I listen to every week because it’s consistently entertaining and informative.

In a world of low management fees, having another scalable source of revenues like a media business could be a differentiator. The cash flows are most likely uncorrelated with markets and there’s an opportunity for ancillary benefits too. For example:

VanEck tapped Dave Portnoy, the founder of Barstool Sports and an online influencer to help launch their Social Sentiment ETF (BUZZ)

At a recent conference, Dan McMurtrie said that his twitter “fame” has helped him with servicing his hedge fund clients

Finally, being able to bounce ideas off a large audience with diverse backgrounds and perspectives helps make everyone smarter

We haven’t seen the banks push very hard into content yet, but that’s starting to change. Some financial institutions have blogs & podcasts that sit outside the paywall, but most of the IP is reserved for clients. The regulatory burden notwithstanding, I think that a few from now years we’ll look back at the JP Morgan acquisition of The Infatuation as the beginning of a big trend. Should incumbent banks adopt a media-forward approach as a means to build trust at scale, increase revenues and lower customer acquisition costs? Demographics and technology seem to be pushing them that way.

P.S. In case you were wondering, yes, a16z has a media business too.

Have a great weekend!