On The Markets Oct. 11, 2021

Signs of a major rotation?

Last week, we didn’t get the systematic vol selling that we’ve grown used to and this is an important development. The absence of these flows might make it more difficult for broader markets to continue their march higher. We start the week with dealer hedge books estimated to be in negative gamma as the S&P 500 remains below the pivotal 4,400 mark. This morning, SpotGamma notes that if we break through 4,375 in the next few days, then it’d be a quick trip down to 4,300. They also calculate that there are 1.4M SPX, 2M SPY & 1.3M QQQ puts set to expire on Friday, which if the market doesn’t breakdown, should provide a buying tailwind into expiry as brokers unwind their shorts/hedges. As a reminder, dealer books in negative gamma makes for choppy markets, which can provide a good tactical trading environment for those who are nimble.

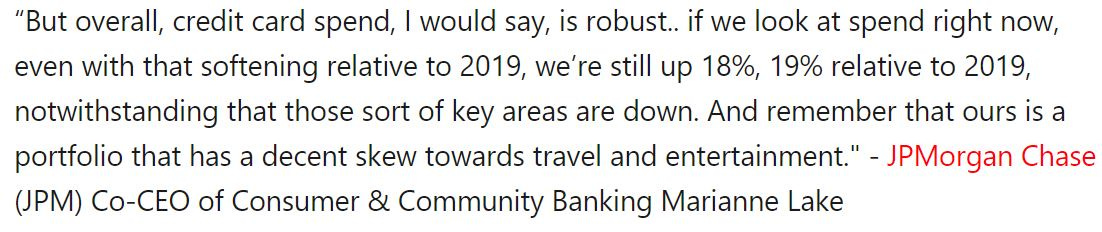

In addition to monthly options roll-off, it’s a big earnings week for the US banks. Most executives have used recent conferences to guide the street, so the actual prints themselves aren’t likely to be anything spectacular. However, analysts are watching for signs & commentary indicative of accelerating loan growth. Any discussion regarding consumer spending will be a focus too as we’re headed into the important holiday season. The street will be hyper-focused on indications of a slowdown related to higher prices, but it seems like the discourse should pave the way for a Santa Claus rally. JP Morgan’s Co-Head of Consumer & Community banking had this to say a few weeks ago:

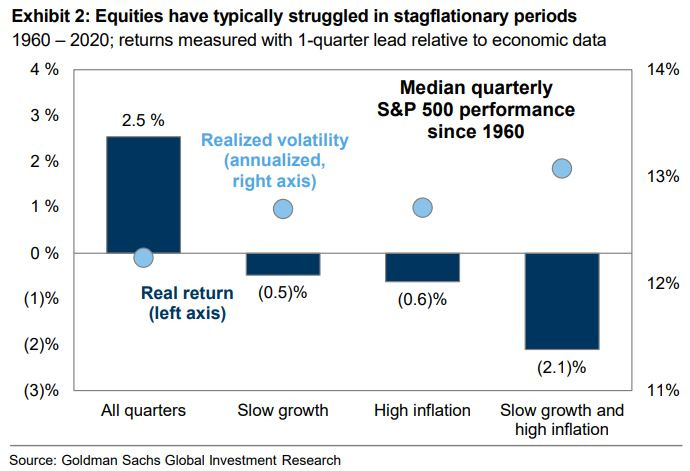

Stagflation was the word of the week as every bulge bracket research department discussed it. It’s been several decades since the markets have had to contend with persistent inflation and slowing economic growth, but as Goldman shows in the chart below, such conditions can wreak havoc on portfolios, so you can see why it’s got the market spooked:

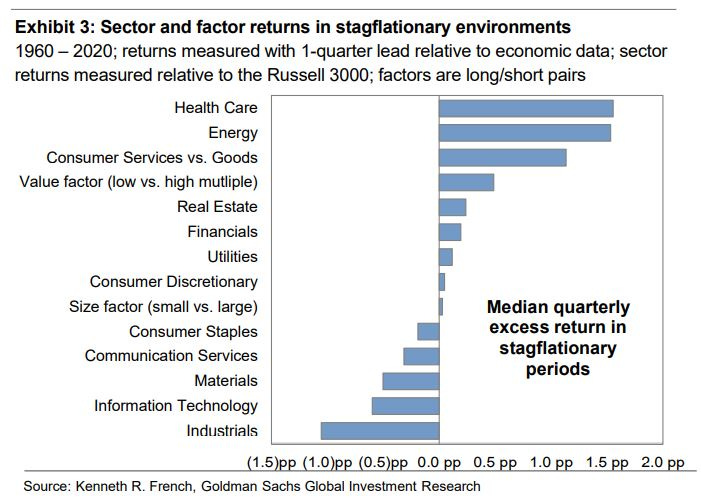

Interestingly, the sectors & factors that tend to hold their own during stagflationary environments have started to show signs of life this year. I think it makes sense to have an allocation to Value, specifically Energy & the Banks. There are many compelling arguments for owning copper-related equities too. Personally, I don’t have any exposure there, but have been mulling over a buy for some time. Last week, GS pounded the table on copper saying that the scarcity is under-appreciated and fears of a slowdown in China are overblown. They forecast almost 15% upside to the commodity with a year-end target of $10,500/t. Overall, it seems like a good time to pick up some commodity-related stocks:

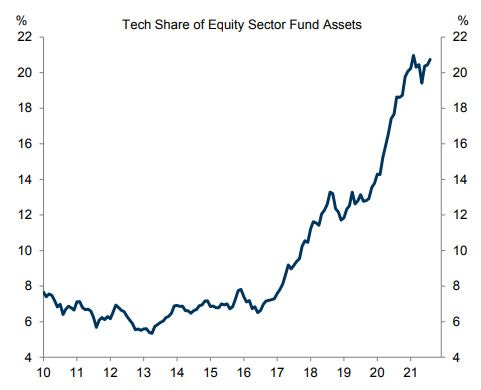

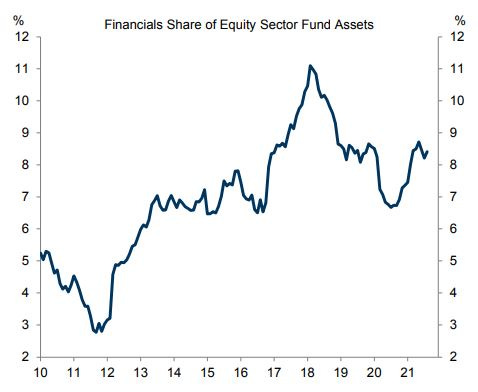

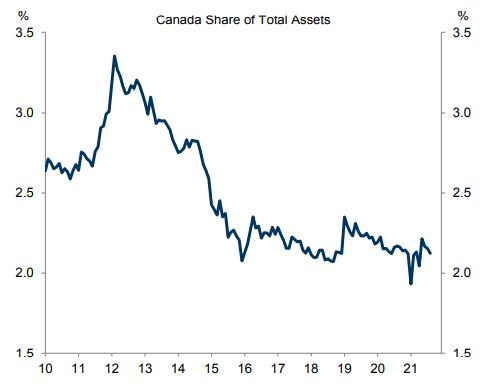

Here are a few more charts that support the idea that we could be at the beginning of a significant rotation in equities:

Technology stocks make up a big part of aggregate stock exposure:

However, commodities are relatively under-represented:

Financials are owned more broadly, but can take some share of allocation if history is any guide:

Canada’s market is well-suited to a recovery in the Value factor:

A couple important points here. The underlying principle of Value investing is that the folks who focus on this factor will sell when the equities approach their estimate of intrinsic worth. Second, the shares commodity extractors have been shown to provide inadequate returns compared to the underlying resources they produce because cost inflation ends up eroding their margins. Historically, there has been poorly-timed & costly M&A too. These are trading stocks. The backdrop is constructive for a continued move higher, but when you take profits, it probably makes sense to deploy them into stocks that have more of a secular tailwind.

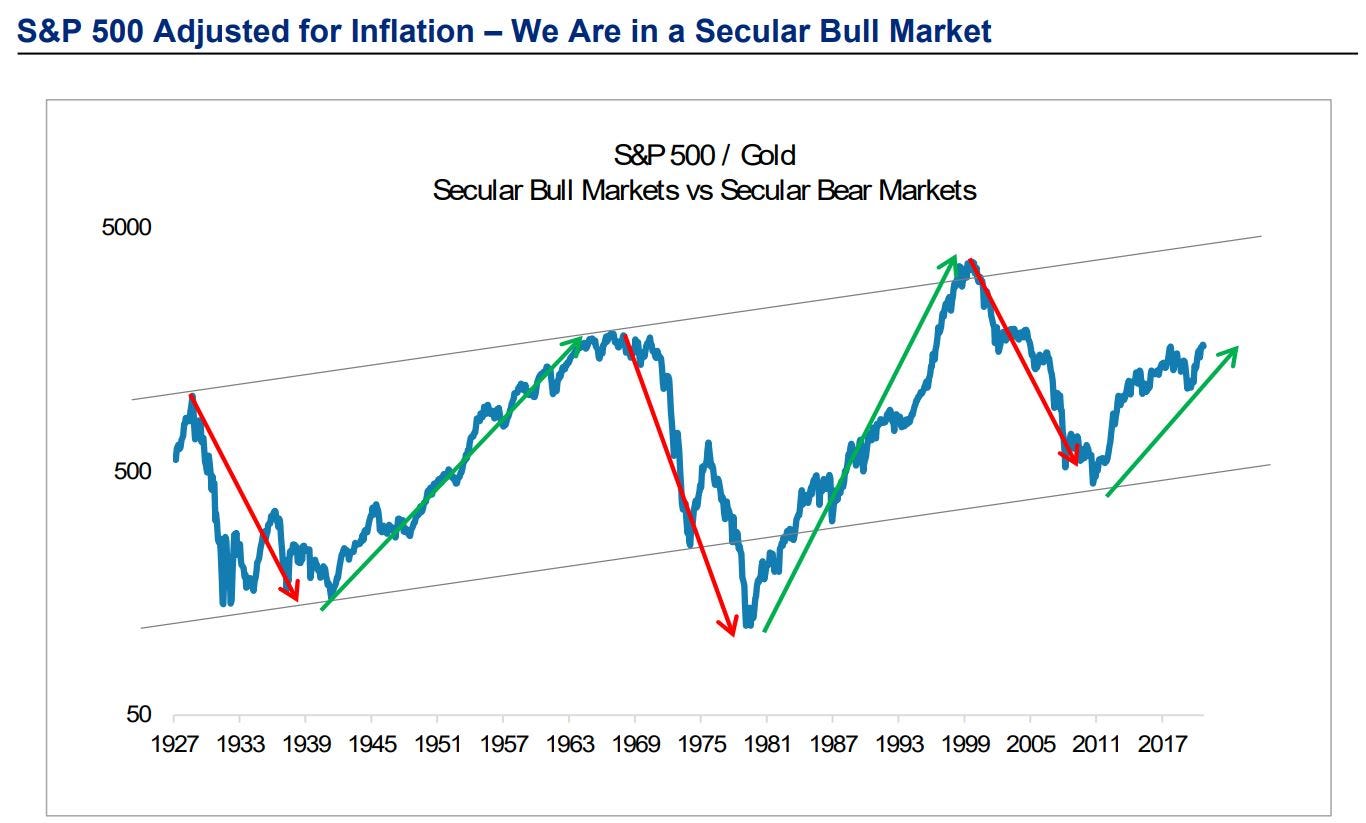

Morgan Stanley remains cautious on equities more broadly and reiterated their call for a 10% pull-back. Current market structure isn’t overly supportive of their position since many have already hedged with puts and vol markets aren’t showing signs of complacency. This is an important week, so we’ll keep you posted if dealer positioning shifts in a bearish way. MS included the graph below in their weekly chart pack, which is a good reminder that even if the longer-term trend is higher, it can be a choppy ride