On The Markets Oct. 25, 2021

Strong funds flow preserves the long bias, but use cheap implied volatility to buy puts

It’s been a couple weeks since we checked in on the market front. We did have a note ready after October options expiry and US bank earnings, but they were largely non-events and our broad view that the Value factor would continue to outperform Growth was unchanged. Frankly, our conviction remains intact, but we’ve come across some interesting content that we wanted to share.

There are a number of tech juggernauts reporting this week, which should add to the noise coming out of Washington regarding budgets/stimulus. The folks at SpotGamma note that dealers are in a considerably lower gamma position on the QQQs, which combined with headline risk could make trading on the Nasdaq relatively choppier. On the S&P 500, they peg support/resistance at 4,525/4,575 and highlight that as long as the we’re above 4,500 then intraday moves should be relatively quiet.

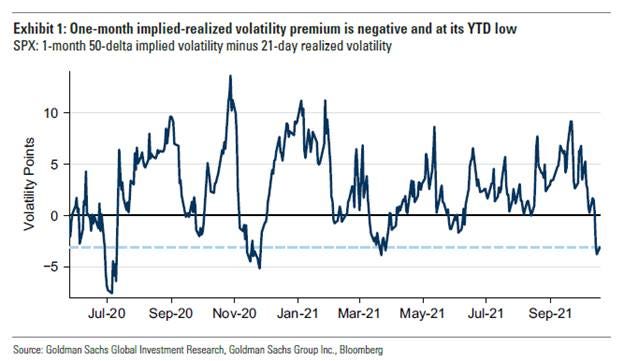

Goldman was out with the following chart last week and remarked that single-stock put-call skew was at its highest level in over a year. This implies that investors are well hedged, so earnings beats are likely to drive a relief rally in specific stocks when they report and the broad index over the following months.

This steep skew also suggests that calls are priced cheap relative to puts in a historical context and it would appear that the Tesla crowd took note today; adding 2.4M calls with about half expiring on October 29th. Dealer hedging likely contributed to the stock’s 12% jump. SpotGamma cautions that:

Thematically, I still like Energy & Banks. The former is a bet on continued producer discipline keeping prices robust and cheap 2022 valuations, while the latter is an economic growth & capital return story. Both seem to provide a good risk/reward setup. Verdad wrote recently that “oil is more a measure of the economic pulse than a driver of it.” While the pundits on TV suggest that high oil prices are a reason to be concerned, you can see that there’s a pretty strong positive relationship between a rising crude tape and equities:

Bank management typically won’t tell you that there’s a problem until after it’s happened and the team at JP Morgan tends to be conservative in their disclosure. The US financials have been guiding to continued economic progress and a fading supply chain glut:

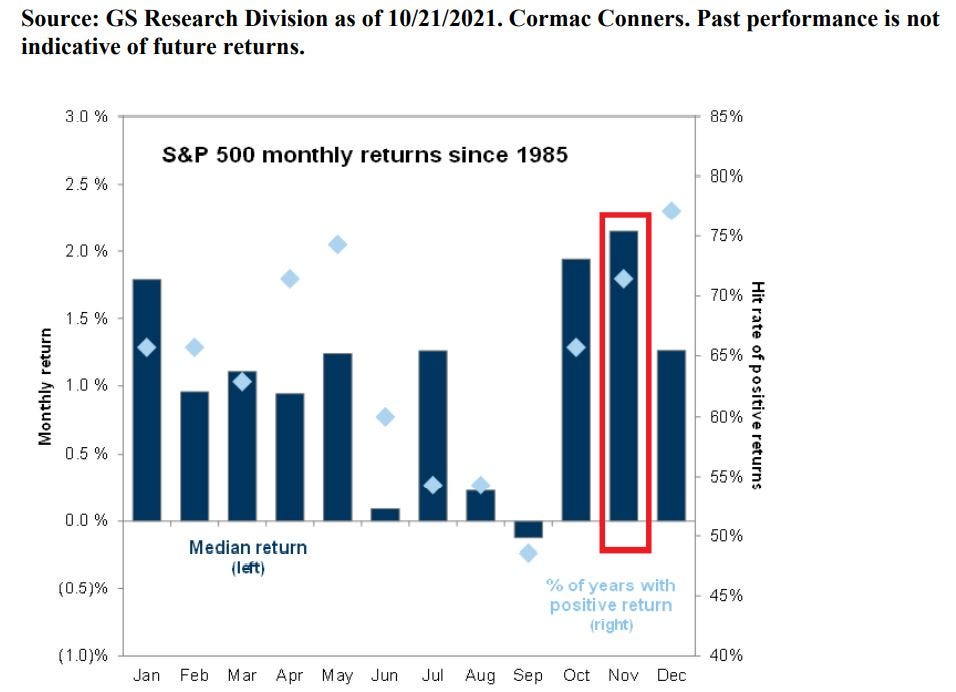

As we progress through the final quarter of 2021, it’s important to be mindful of seasonal funds flow and the associated returns:

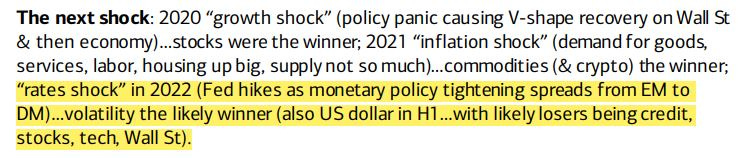

Stronger economic prospects combined with waning inflation pressures from loosening supply chains would support equity markets. However, it would also coincide with a more hawkish stance from the Central Banks. Given the size and scope of the stimulus provided, we can expect markets to fear a policy misstep as the punch bowl is withdrawn. BofA is calling this the 2022 “rates shock”:

Bringing it all together, if I was drawing up a tactical playbook given the information we have today, then it seems important to stay long the economically sensitive sectors (with a personal preference towards energy & financials) as we head into 2022. Assuming markets climb the wall of worry and vols drift lower, then I think a good trade will be to buy puts &/or raise cash before liquidity dries up for the holidays. Ultimately it seems like markets can have another good year, but there are considerable rebalancing activities that coincide with the turning of the calendar and that often coincides with volatility.

If we do get a “rate shock” early next year, then I think that’d be a good opportunity to pick up some of the secular growth stocks with the cash you raise in December through long sales or by monetizing the puts you picked up. This year it’s been helpful to take a barbell approach to equities, which involved owning Growth & Value and rebalancing as relative performance required. It seems that this would be a prudent allocation in 2022 as well.

Things likely won’t work out as we’ve outlined above, but that’s our current operating model. As always, we’d love to get your take on these ideas or markets in general.