We’d like to try something a little different at Onsight for a bit. Some subscribers have asked for more trading-related color, so in addition to sending longer notes on Friday/Saturday that are thematic, we’ll circulate some more tactical views too. This newsletter is a work in progress, so any feedback would be helpful – we’re in this together.

On Friday, the folks at SpotGamma believed that significant vol selling and a bull-biased put-call ratio of 1.48 on had pushed dealer books to carry significantly less negative gamma. However, this morning, they’re calling for continued choppiness since the S&P 500 is below the 4,380 “vol trigger” or resistance line. We’re setting up for a very choppy week. If we can push through 4,400 then positive gamma takes over and dealer hedging flows would suppress intraday moves. This would generally be supportive of higher prices. They see support levels around 4,300 or right about where we’re sitting now. This is an important level to hold. Interestingly, the VIX isn’t spiking through last week’s highs on this morning’s selling... Also on the options front, I thought this thread provided an impressive plain-language description of the mechanics of a large put-spread collar that was rolled last Thursday and how it can impact daily flows.

There were a couple of notable reports out from the bulge bracket banks over the weekend which provide a backdrop to the macro narratives that are battling it out these days. No one ever knows what’s going to happen, but it helps to have an idea of the likely scenarios and popular viewpoints:

In his weekly piece, Morgan Stanley’s cross-asset strategist, Mike Wilson, outlines the firm’s framework for evaluating equity markets, which is focused on the rate of growth and valuation. As it relates to the latter, MS’ process is based on the idea of a cyclical market and tends to make use of historical analogies. Rounding out their high-level perspective is technical analysis. Bringing those elements together, the team arrives at the following:

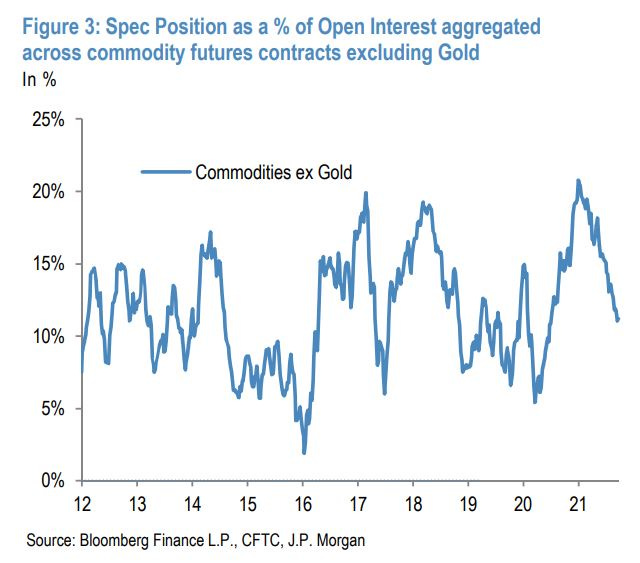

JP Morgan’s flow group believes that the bull run in commodities is still intact and strikes a cautious tone on equities too. The note goes into considerable detail, but here’s what I think is the important takeaway: as it relates to positioning, there’s more buying potential in the commodity space relative to equities. Stocks that have exposure to metals, oil & gas, etc. can likely outperform, but remember that in a sell-off correlations go to one. This can be an opportunity. It’s always critical to keep our trading timeframes in mind. Tactically, it seems like buying resource-based stocks on pull-backs seems to be a winning move as we head into 2022. The reasoning is two-fold:

o In a historical context, institutional investors aren’t overweight resources. Given the strong backdrop for higher commodity prices, this could be a buying tailwind

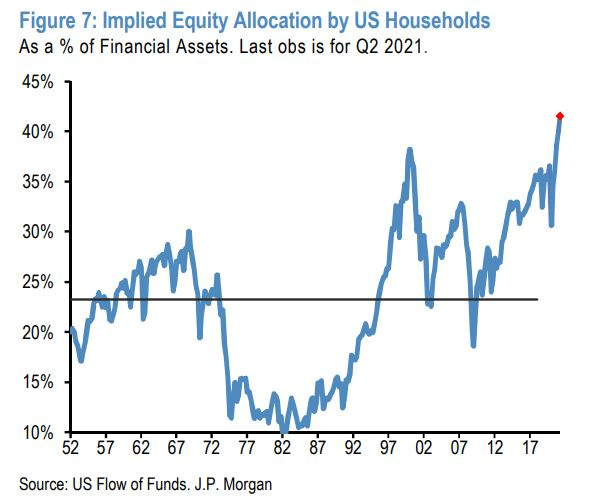

o As it relates to the broader equity markets, an important new source of buying since the pandemic has been retail. Taking a page out of the history books, it seems that the pace of such purchases could peter out:

At the very least, the risk/return profile of owning stocks appears like it could be improved by owning names with positive commodities exposure

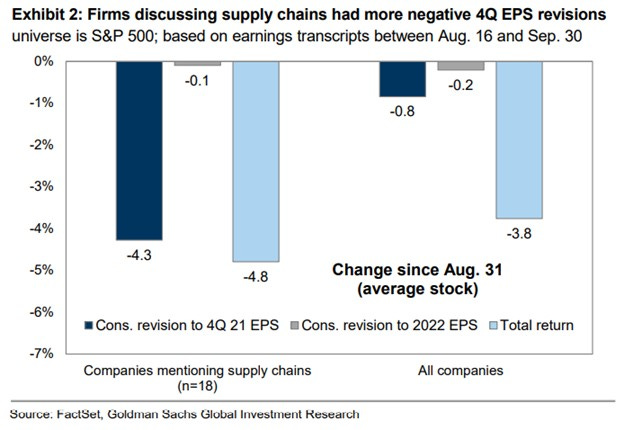

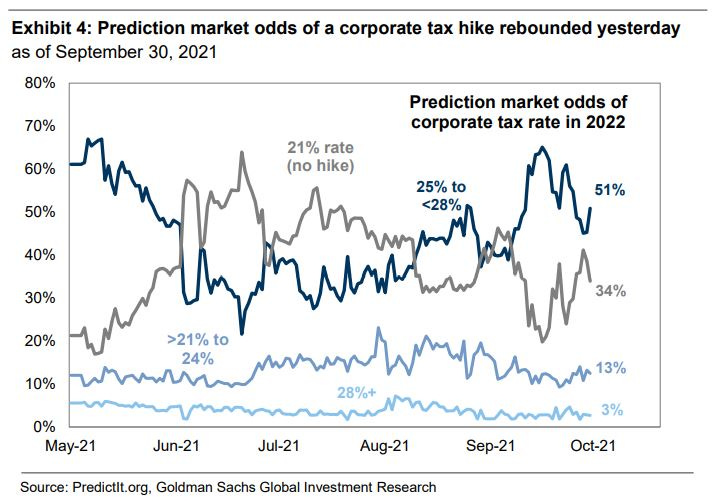

Finally, let’s turn to the equity team at Goldman who published a good earnings preview. They take the view that there’s upside to consensus estimates but expect the frequency and magnitude of EPS beats will moderate from what we witnessed during the first half of the year. The strategists there are also focused on the impact of tighter monetary policy and supply chain constraints. As such, they’ll be focused on commentary during conference calls that relates to supply chains, oil, labor costs and China growth rates. At current prices, the strategists believe most of the risks here are contained (which is in contrast to Morgan Stanley), but how management teams guide to future profitability will be a key performance differentiator. They add that uncertainty around corporate taxes is an additional headwind for next year

Bringing this all together, the current environment probably deserves some respect in the form of caution.Time horizon matters most here. If you’re managing money for the long term, then most of what is included above falls under the noise category and you can use any weakness to pick up your favorite names on the cheap. On the other hand, if the bag you’re allocating is more tactical, then it’s important to be mindful of the risks & not try to be a hero. We’ve broken through the 100-day moving average on the S&P 500 for the first time in a year and the 200-day is another 3.5% away…

One of the biggest advantages that non-professional investors have over the folks who charge fees is that they can hold greater levels of cash. While my portfolio is still positioned in anticipation of higher prices, I think we’ve entered a different market regime where “up only” cedes to “white water rafting”. This can provide exceptional opportunities to pick up shares of great businesses, but it’s not the time for running a high margin balance. If you fancy being nimble, then maybe look to pick up some banks &/or oil companies in this current weakness – they should provide some nice torque to the upside. Having said that, I’d be curious to get your thoughts. Should we be all-in and if so, in which sectors/names?