On The Markets Oct. 7, 2021

Are we about to gamma flip?

At the time of writing, we’re flirting with 4,400 on the SPX, which has been an important resistance line and (not coincidentally) represents the level at which SpotGamma estimates option dealer books switch from negative to positive gamma. As a reminder, when positioning flips to the latter, it means that brokers will sell into rising markets & buy dips. This behavior has the effect of dampening volatility, which is typically conducive to a grind higher due to Vanna & Charm. I don’t want to get into the calculus, but consider those to be variables for hedge requirements due to changes in vol and the passage of time. What does it all mean? Above 4,400 dealer hedging flows are expected to be supportive of a rising market. With some of the headline risks being pushed out (mostly the debt ceiling & Evergrande to an extent) additional dip-buying from the institutional crowd is likely another source of higher prices and anyone who tried to short that dip will likely be covering. The path for markets seems to be higher, but first we need to break resistance.

JP Morgan’s Marko Kolanovic maintained his positive disposition to equities yesterday, urging clients to buy the dip in all cyclical assets (domestic & emerging markets) except Tech. To summarize, he believes that the 4th COVID wave will be the last of real significance, so the reopening trade has pushed through a significant headwind. This implies “intensifying energy issues, rising inflation and bond yields.” In such a world, tactical allocators would likely do well to own “energy (equities and commodity), materials, industrials and financials, and reopening, COVID-recovery, reflation and consumer themes.” They’re cautious on technology names due to relatively high valuations & extreme overweighting in portfolios.

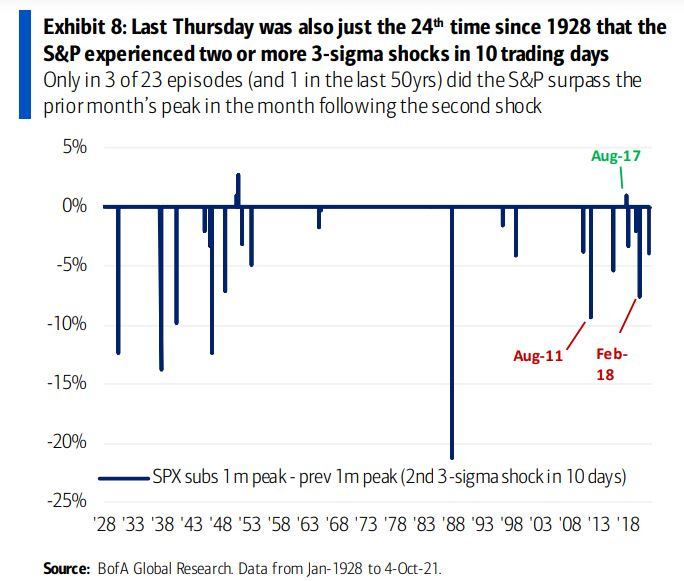

Interestingly, Bank of America’ EQD group was out with a piece outlining their view that investors are losing faith in buying every dip. On their math, the most recent market weakness saw the S&P 500 post two 3-sigma downside shocks:

Going back 50 years, markets have reached new all-time highs in the subsequent month only once after two or more episodes like this. BofA anticipates markets grinding lower over the next few months without vols blowing out.

Both groups can be right though. Energy & Materials make up 2.9% and 2.5% of the S&P 500 respectively, so they really have to move in order to offset weakness in Info Tech at 27.6%. For context, the weights for Financials & Industrials are 11.6% and 8.1% respectively. Personally, I think the energy names are interesting as their commodity hedges roll off in 2022 and free cash flow priorities remain skewed to shareholder returns. It can be anticipated that capex will move higher, but management teams seem committed to staying disciplined for now… Banks also look good as they’re beneficiaries of rising rates and regulators should let them ratchet up dividends & buybacks as the pandemic fades.

The 2022 landscape looks like it will be characterized by negative EPS growth forecasts for the broad-market, monetary stimulus withdrawal and meandering government policy. As such, it probably makes sense to keep some cash on the side or at least keep margin balances low. Overall, it’s important to stay invested, but after the run we’ve had I think a bit of tactical buying power makes sense. Morgan Stanley’s Andrew Sheets published a two-part ode to cash recently and here’s an excerpt highlighting a few of the reasons why cash isn’t trash:

Resource-based stocks are volatile enough as it is, so I’m not convinced you need to lever up & YOLO those. Banks are a bit sleepier, but on a total return basis I suspect you’ll be pleased to have owned them 12 months from now. What do you think?