You're Gonna Need a New Map

David Einhorn, Value Investing, Momentum & Incentives

I participated in Simplify’s Entering The Fall - Thought Leadership Series on Monday, which featured a number of high-profile guests from across the investment industry. Many of the topics discussed will serve as a framework for this week’s note, but there’s a bunch I don’t go into, so let me know if you’d like to chat more about my takeaways – it was a pretty interesting day.

David Einhorn kicked things off on a downtrodden note. It’s been a tough road for the Greenlight Capital founder since he made headlines for a well-publicized bet against Lehman Brothers just before the Great Financial Crisis. You have to give him credit for sticking to his guns, but long/short value investing remains an unloved strategy following more than a decade of underperformance. With humility, David admitted “I would fire myself” and explained that the firm was in the midst of a significant restructuring due to persistent redemptions.

When speaking about his skill as a short seller, Einhorn’s peers used to say things like “there here is a mythology around him” as he was cunning at dissecting a company’s disclosures, wasn’t afraid to go against the grain & took concentrated bets. These attributes have remained consistent and broadly, the Greenlight process has remained the same as well:

That quote is from 2018 and the fund has continued to struggle since. What happened? It seems like a case of the Map & Territory Problem at work. Here’s an abstraction about retail legend, Ron Johnson’s hiccup at JC Penny:

As you can imagine, there were a number of factors contributing to Einhorn’s struggles and Institutional Investor provides a good summary. One thing the author touches on is the idea that buying stocks with low valuations & selling ones that screen expensive has faltered as a strategy more broadly. This got me thinking about a note I read from KCB’s Tom Morgan recently about “morphic resonance” or a collective intelligence that somehow permeates across a community and everyone gets “smarter”

You can’t argue with the facts & Momentum has been a winning strategy. However, the idea of price reflecting all information is a bit too “Efficient Market Hypothesis” & there have been countless examples of speculative zeal getting out of hand. The idea of humanity getting collectively smarter is sometimes called the Flynn Effect, which refers to a general trend higher in standardized IQs over time. While the ways of Ben Graham were once esoteric, cash flow-based equity analysis and intrinsic value is now covered in almost all investment courses. Borrowing from Morgan, perhaps seeking out cheap stocks (& buying the dip?) has crept into our collective consciousness. Nowadays you need more to have an edge:

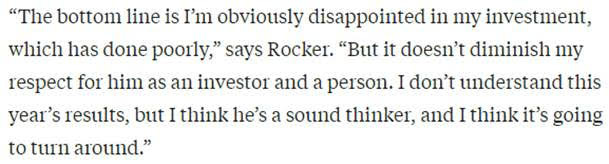

If Value investing has underperformed for so long, then why has it remained popular? Anecdotally, I’d argue that its contrarian nature is fundamentally appealing. It would make sense that sponsorship from the great Buffett & Munger has had an influence too. Further, the relationship-based nature of our business has likely had an impact. Take this comment about Greenlight after almost 10 years of underperformance:

*David Rocker

Another hedge fund manager at the Simplify conference was Dan McMurtrie of Tyro Partners. He emphasized how his business is one of narratives and this extends to the client relationship. Part of the excess return earned by hedge funds comes from taking concentrated positions – sometimes in illiquid stocks. If a client grows uncomfortable with the associated risks in the middle of a downturn, then they could panic & request a redemption. The selling pressure would be an additional performance headwind at the expense of the other capital providers. There’s a circularity between managers & clients that requires careful consideration. Super Mugatu said they spend 6 – 36 months screening potential clients. You can imagine that this kind of sales process doesn’t scale well & Mychal Campos of Betterment (a robo advisor) was on hand to confirm as much. This is just an outsider’s perspective, but it seems that there’s a divergence in priorities between the strategy and the client at Greenlight vs Tyro.

A “value investing death spiral” has been described as a situation when momentum funds continue to gather assets, which perpetuates the underperformance of laggards. As capital providers grow tired of the poor results, they redeem. This adds to the flows headwind on the already “cheap” names and so on. Over time, this cycle has the ability to build up a sort of potential energy in otherwise good businesses that might not get picked up by a systematic investment screen for whatever reason. The problem, of course, is trying to time when the coiled spring will break loose.

During the Simplify conference, Einhorn mentioned that some of the Greenlight portfolio companies on the long side are likely to generate free cash flow over the next few years equal-to or greater-than their current market caps. On the surface, this seems positive, but the shares didn’t react when management revealed their intentions to launch large buyback campaigns. Mike Green, who hosted the event, is a vocal critic of letting Passive investing get too big & his reasoning for Einhorn’s underperformance is tied to the idea that market structure has changed and flows matter more than fundamentals.

Let’s consider an analogy… In the wake of the oil price rout that effectively spanned from 2015 until earlier this year, capital investment in the energy patch fell off a cliff. The story was double-sided, as initially the world was awash in supply & then the pandemic impaired demand. We’ve seen a dramatic rise in commodity prices as mobility trends recover, but producers continue to prioritize shareholder returns and investment in greener technologies. As consumers start to feel the pinch of higher gas prices at the pump, do you think it’s inevitable that the industry will be criticized for buying back shares instead of drilling wells? Given all the fanfare around ESG, the irony here runs deep, but let’s look past that for now.

Using Exxon Mobil as a proxy for the E&P biz, it’s interesting to see that the cost of capital varies positively with the price of crude. Algebraically, this makes sense because as the company’s market cap shrinks the weight of equity in the WACC calculation would decrease and I guess this is only partially offset by the higher beta during a sell-off.

The cost of capital is the inverse of a valuation multiple, so in a way, this speaks to investors’ general risk aversion. XOM tends to trade at a lower multiple (higher WACC) when the oil price is robust. This might imply market concerns about the sustainability of cash flows & vice versa. Now let’s think of this from a capital budgeting perspective. When the oil price is elevated, so too is the company’s cost of capital and this higher hurdle rate should make it more difficult for projects to be approved. Conversely, when prices are subdued, the bar for deciding to drill, in theory, is lower. In practice, the opposite happens as producers pursue growth during high price regimes & retrench in deflationary environments.

The energy industry (like most commodity players) has been criticized for not earning their cost of capital in the past. This was even before ESG moved to centre stage and empirically increased the funding cost. From a stakeholder perspective, market forces have incentivized companies to prioritize returning capital to shareholders over drilling wells. David Einhorn discussed this paradox too and said his conversations with management teams revealed that they’d prefer to operate & grow their businesses. We can see that the story is more complicated that what price/momentum would suggest. It’s also notable that vacuums of capital can provide excellent return opportunities.

I’d like to close the loop with something a bit controversial… What if we consider David Einhorn as a contrarian indicator. I mean no disrespect here and would be thrilled to have enjoyed a small fraction of the man’s success, but let’s call a spade a spade – you’d have done well to have reversed his portfolio over past decade & change. Greenlight was short names like Netflix & Amazon, while being long General Motors. However, after almost 15 years of stubbornly struggling, he’s beginning to adapt… In Greenlight’s Q2-2021 letter Einhorn wrote: “The performance of our short portfolio in 2020 and in early 2021 was unacceptable, so change is certainly needed. If we swing a little less hard, we should hit more balls.”

The conference concluded as Mike Green interviewed Josh Wolfe – a VC at Lux Capital who said that VC wouldn’t be an asset class he’d be contributing more to right now. All of his discussions with peers are about how great everything is, which has tended to foreshadow tougher times. I saw this note recently:

That seems a bit lavish, which contrasts interestingly with a die-hard value investor’s nihilism. We’re seeing a dynamic at play in the public markets where old school industries are starting to catch a bid and technology is selling off. There have been many head fakes over the years, but could this be a legitimate inflection point? I’d love to get your thoughts.

Have a great weekend!